1. What is CbCR?

Country-by-Country Reporting (CbCR) is a global tax reporting framework established by the OECD as part of the BEPS (Base Erosion and Profit Shifting) initiative.

Its primary purpose is to enhance transparency by requiring large multinational enterprises (MNEs) to disclose a comprehensive breakdown of their global operations. This includes key financial data—such as revenue, profits, taxes paid, and employee counts—for every jurisdiction where they conduct business. Essentially, it provides tax authorities with a clear overview of how profits and taxes are distributed worldwide.

2.When is the CbCR (Country-by-Country Reporting) obligation triggered?

In accordance with the Adjustment of International Taxes Act in Korea, a CbCR obligation arises under the following conditions:

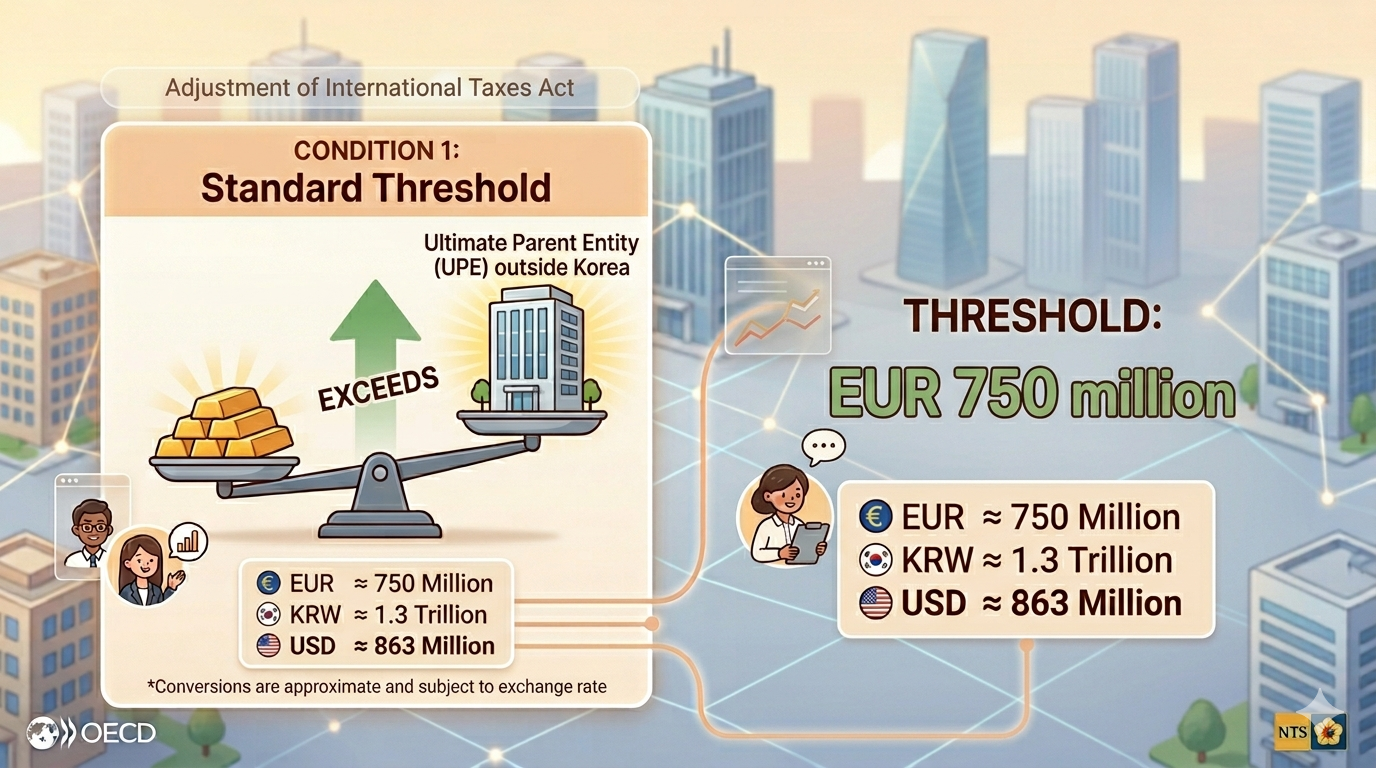

Standard Threshold: If the ultimate parent entity is located outside of Korea and the consolidated group revenue exceeds EUR 750 million (approximately KRW 1.3 trillion) in the preceding fiscal year.

*EUR 750,000,000 = USD 863,138,456.44 = KRW1,302,907,500,000

Local Law Compliance: Even if the figures slightly differ, the obligation is also triggered if the ultimate parent entity is required to file a CbCR under its local jurisdictions’ laws, provided their specific revenue threshold is met.

| (1) | The following taxpayers shall submit a Master File, Local Files, and Country-by-Country Reports prescribed by Presidential Decree regarding their business activities, the details of transactions, etc. (hereinafter referred to as "consolidated report on international transaction information") to the head of a tax office having jurisdiction over the place for tax payment within 12 months from the end of the month in which the end date of the business year under Article 6 of the Corporate Tax Act falls, as classified in the following: |

| 1. | A taxpayer who meets the requirements prescribed by Presidential Decree, in terms of the turnover and the volume of international transactions with a foreign related party: A Master File and Local Files; |

| 2. | A taxpayer who meets the requirements prescribed by Presidential Decree, in terms of turnover, etc.: Country-by-Country Reports. |

| (1) | "Taxpayer who meets the requirements prescribed by Presidential Decree" in Article 16 (1) 2 of the Act means taxpayers classified as follows: |

| 1. | Where the ultimate parent company prescribed by Decree of the Ministry of Economy and Finance (hereafter in this Article referred to as "ultimate parent company") is located in the Republic of Korea and the turnover in consolidated financial statements for the immediately preceding taxable year exceeds one trillion won: The ultimate parent company in the Republic of Korea; |

| 2. | Where the ultimate parent company is located in a foreign country and the turnover on consolidated financial statements for the immediately preceding taxable year exceeds the following amounts: A related company prescribed by Decree of the Ministry of Economy and Finance in the Republic of Korea (hereafter in this Article referred to as "domestic related company"): |

| (a) | Where it is obligated to submit a Country-by-Country Report under the statutes or regulations of the country in which the ultimate parent company is located: The amount prescribed by the relevant statutes or regulations; |

| (b) | Where it is not obligated to submit a Country-by-Country Report under the statutes or regulations of the country in which the ultimate parent company is located: 750 million euros. |

3. Who is required to file the CbCR?

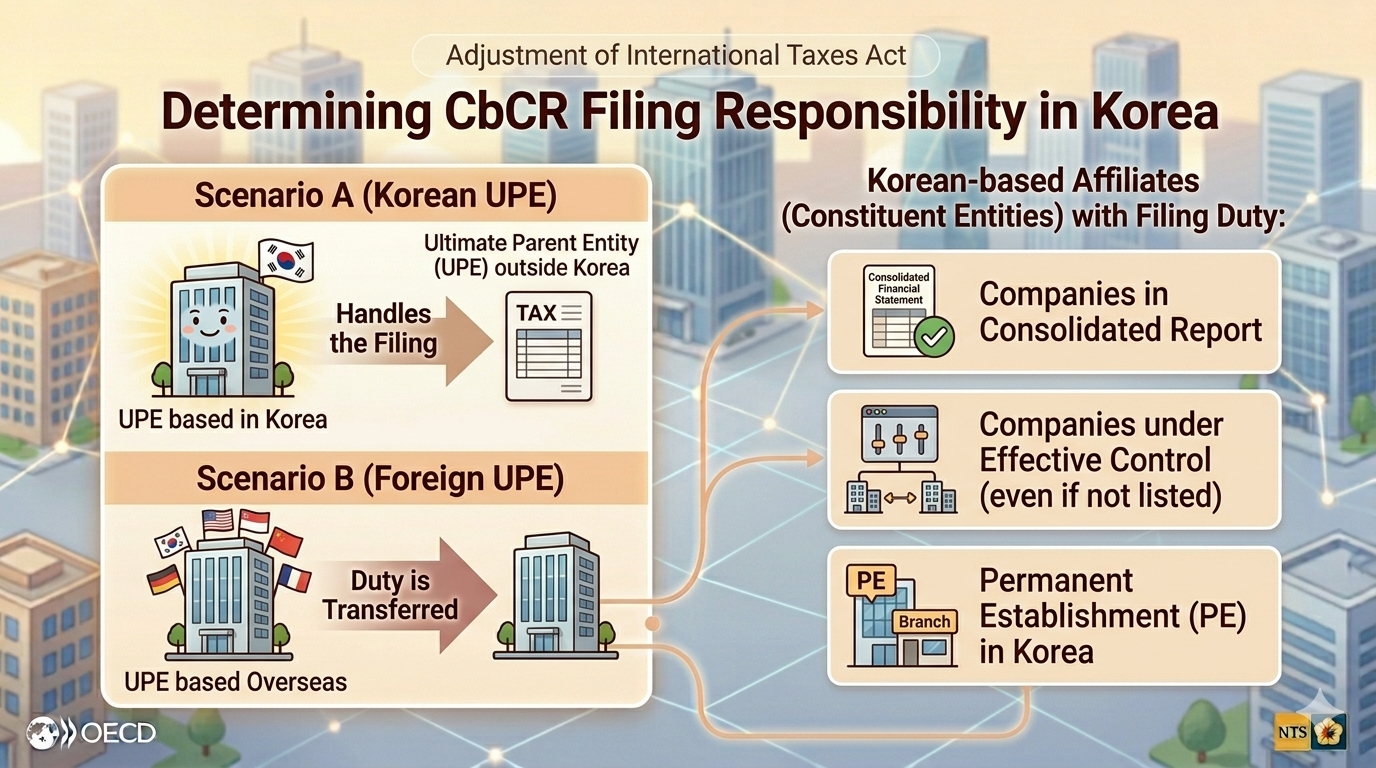

Determining who must file the report is a key step in compliance. If the "head" of the corporate group (the Ultimate Parent Entity) is a Korean company, that parent company handles the filing. However, if the parent is based overseas, the Korean-based affiliate must take on this duty.

To clarify, the Korean entities (often referred to as Constituent Entities) that fall under this requirement include:

- First, any company that is part of the group's consolidated financial report.

- Second, companies that the group effectively controls, even if they aren't officially listed in the consolidated statements.

- Lastly, any branch or office that qualifies as a Permanent Establishment (PE) in Korea.

| (1) | "Taxpayer who meets the requirements prescribed by Presidential Decree" in Article 16 (1) 2 of the Act means taxpayers classified as follows: |

| 1. | Where the ultimate parent company prescribed by Decree of the Ministry of Economy and Finance (hereafter in this Article referred to as "ultimate parent company") is located in the Republic of Korea and the turnover in consolidated financial statements for the immediately preceding taxable year exceeds one trillion won: The ultimate parent company in the Republic of Korea; |

| 2. | Where the ultimate parent company is located in a foreign country and the turnover on consolidated financial statementsfor the immediately preceding taxable year exceeds the following amounts: A related company prescribed by Decree of the Ministry of Economy and Finance in the Republic of Korea (hereafter in this Article referred to as "domestic related company"): |

4. How and When to File the CbCR

Reporting your CbCR involves two main stages to ensure the tax authorities have a clear picture of your global operations.

First, the report itself should cover essential financial metrics for each jurisdiction, including profits, tax payments, and a description of primary business activities. It’s important to provide this data accurately to reflect your group’s economic presence in each country.

Regarding the timeline, please keep two important dates in mind:

- Within 6 months: You need to file a Notification to inform the authorities which entity will be responsible for the main filing.

- Within 12 months: The final CbCR report must be submitted.

Missing these deadlines can lead to unnecessary complications, so we recommend preparing these documents well in advance of the fiscal year-end.

| 3. | Country-by-Country Report: A report which includes the following matters about a taxpayer who falls under Article 16 (1) 2 of the Act and the MNE group, etc. in a special relationship prescribed by Decree of the Ministry of Economy and Finance with the taxpayer: |

| (a) | Details of profit by country; |

| (b) | Pre-tax profit or loss by country; |

| (c) | Amount of tax payment by country; |

| (d) | Capital by country; |

| (e) | Major business activities by country. |

5. How to Qualify for a Reporting Exemption

We understand that preparing a CbCR is a significant undertaking, as it demands granular financial and operational data from every single group member. Fortunately, Korean tax law provides a practical exemption to avoid double reporting.

Essentially, a Korean subsidiary does not have to file the full report itself if it can demonstrate that another group entity is handling the task. To qualify for this:

- File a Notification: You simply need to notify the Korean tax authorities about which foreign entity will be submitting the CbCR on behalf of the group.

- Verify the Treaty: The country where that reporting entity is located must have an active tax information exchange agreement with Korea.

By coordinating with your global headquarters and ensuring these administrative steps are taken, you can significantly reduce your local compliance workload.

Article 35 (Submission of country-by-country report)

| (2) | A domestic ultimate parent company and a domestic related company shall submit (including submission via the information and communications networks) data prescribed by Decree of the Ministry of Economy and Finance, which are about a person obligated to submit a Country-by-Country Report, to the head of the tax office having jurisdiction over the place for tax payment, within six months from the last day of the month in which the end date of each fiscal year falls. |

| (3) | A domestic related company which has submitted the data under paragraph (2) by the deadline for submission need not submit a Country-by-Country Report in any of the following cases: |

| 1. | Where it is obligated to submit a Country-by-Country Report under the statutes or regulations of the country in which the ultimate parent company is located and such Country-by-Country Report is exchanged with the Republic of Korea according to a tax treaty; |

| 2. | Where another domestic related company submits a Country-by-Country Report representatively; |

| 3. | Where the ultimate parent company requires a related company located in a third country to submit a Country-by-Country Report to the relevant country on its behalf and such Country-by-Country Report is exchanged with the Republic of Korea according to a tax treaty. |

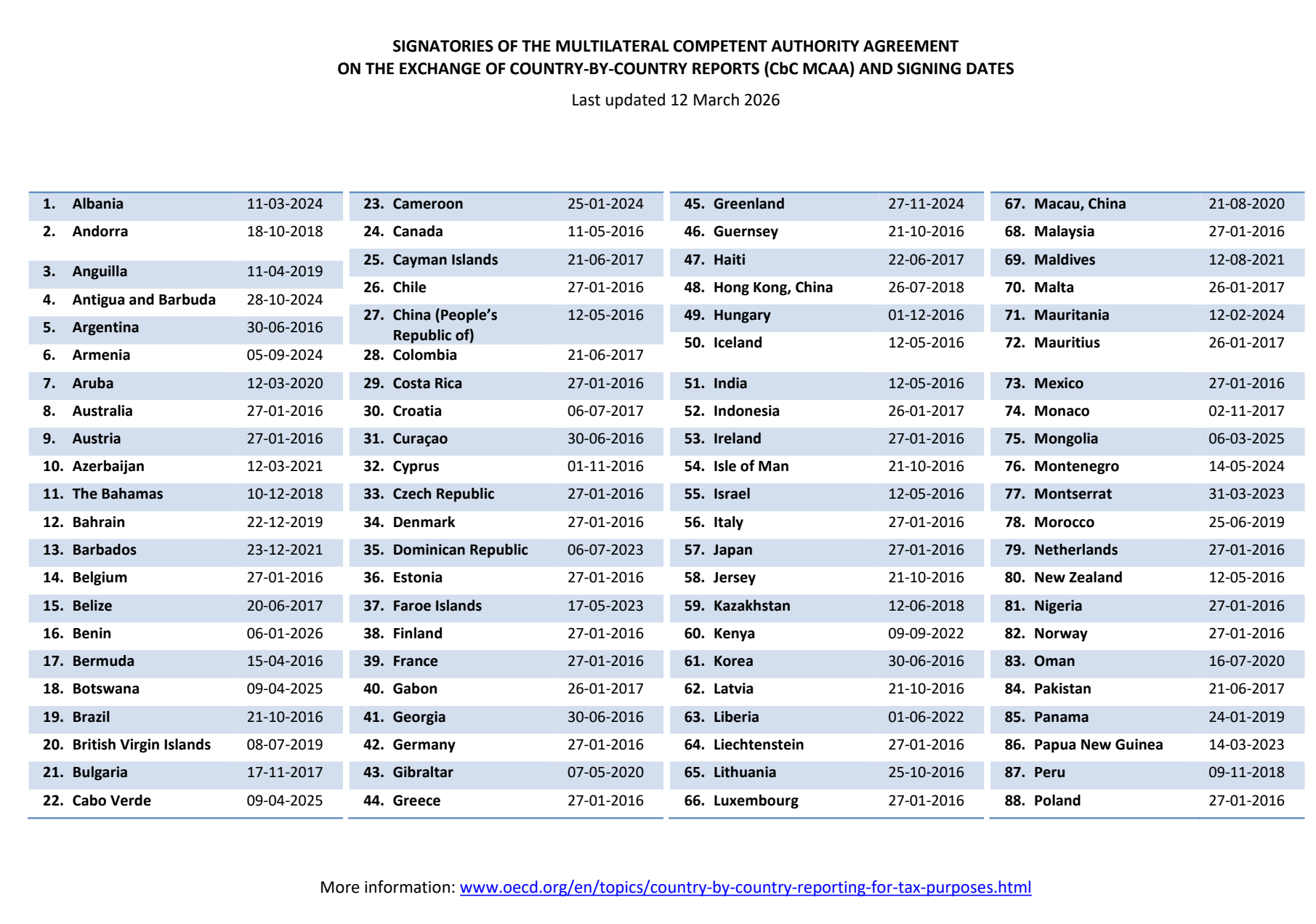

6. Which Countries have a CbCR exchange agreement with Korea?

One of the most frequent questions we receive is whether a specific country is included in the exchange network. You'll be pleased to know that South Korea has established CbCR exchange relationships with 114 countries worldwide.

This list is quite comprehensive and covers the vast majority of countries that conduct business with Korea. For instance, China, France, Italy,and Etc.

If your group's Ultimate Parent Entity is located in any of these major jurisdictions, you can likely streamline your local compliance. For a complete and up-to-date list of all 114 countries, you can always refer to the official announcements from the National Tax Service (NTS) or the OECD's status of signatures page.

'Corporate income tax filing' 카테고리의 다른 글

| It's time to get ready for the 2nd VAT return filing. (0) | 2025.01.13 |

|---|---|

| How Companies Share Their Earnings with Shareholders in Korea: The Dividend Process (0) | 2024.12.30 |

| What’s the Difference? Tax Invoice vs. Regular Invoice (0) | 2024.12.16 |

| Foreign Corporations Should Be Careful When Borrowing Money from HQ (Thin Capital Taxation) (0) | 2024.11.28 |

| Donations can cut your company tax. (2) | 2024.10.23 |